Practical Summary:

- Of all of the beaten down tech stocks that have taken their lumps since November, this is the one that Ben Graham would pick.

- Meta is no longer a compelling “growth” story, but it will make an excellent “value” play once it rotates to investors who like that kind of thing.

- With a free cash flow yield of over 6% (twice that of the NASDAQ 100) and optionality in Reality Labs, growth is no longer necessary to deliver solid shareholder returns.

Since Thanksgiving, US public stocks have experience a fierce rotation from high-flying growth stocks to good old-fashioned “value stocks.”

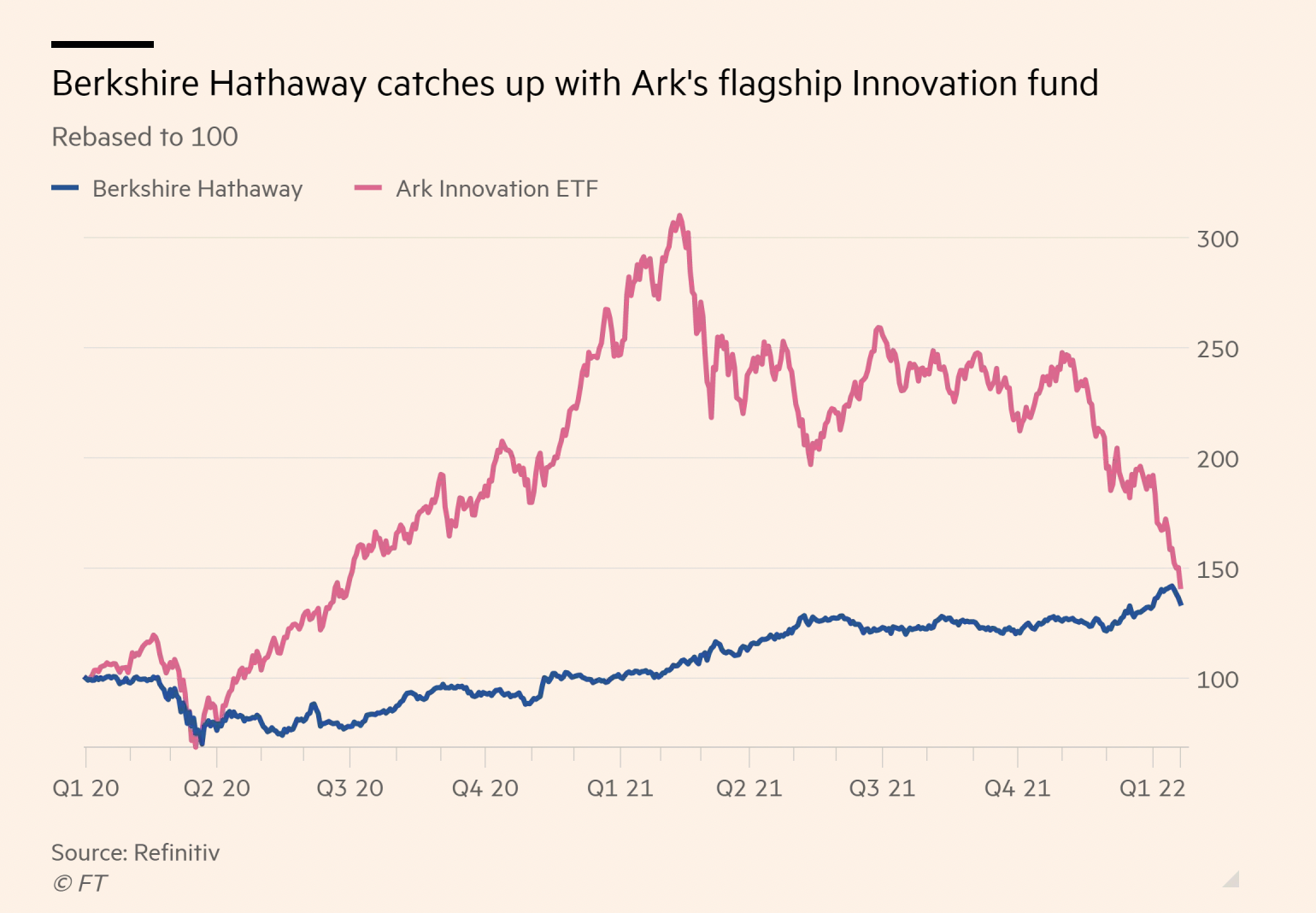

Take the diverging performance of two prominent investors who embody two very different styles. Cathie Wood runs ARK Invest ETF (NASDAQ: ARKK) and aggressively chases fast-growing, bombastic, disruptive companies like Tesla, Zoom, Coinbase, and Roku. Warren Buffet’s Berkshire Hathaway Inc. portfolio (NYSE: BRK.B) consists of cash-flowing financial services and banks (e.g., GEICO, Bank of America), railroads, profitable and durable consumer retail brands (e.g., Coca Cola and Kraft), jewelers, carpet manufacturers, and Apple.

Wood’s heart-pumping, pulse-racing portfolio has dropped by 40% since November 1, while Buffet’s plodding group has edged up by 12%. Since the start of the pandemic in March 2020, their performance is about even (ARKK has a slight lead, with a 43% appreciation versus 34% for Berkshire), though ARKK investors must feel like they’ve been on a rollercoaster ride.

Chart 1: The Hare and the Rabbit

Meta’s Q1 Earnings Release

This brings us to Meta Platforms, Inc. (NASDAQ: FB), the parent company of Facebook, Instagram, and WhatsApp. After its Q1 earnings release, Meta got hammered. In the four trading days after their earnings release on February 2, the company’s stock experienced a once-in-a-lifetime, epic beating. First, it shed almost $237 billion in market cap overnight, dropping by 26%. Then the stock fell further over the next three trading days, by another 7%, bringing the total post-earnings drop to 32%.

That brings Meta’s overall decline from last year’s 52-week higher to 40% (the share price had actually held quite well relative to other tech stocks from November all the way up until February 4).

What Happened?

If you are a growth investor, here’s what I saw in FB’s earnings that was concerning:

First, Facebook’s global daily active users declined from the previous quarter for the first time, to 1.929 billion from 1.930 billion.

Second, Q4 revenues were up +20% YoY (to $33.7 billion), but Q1 guidance was for +3-11% growth. After consistently growing revenues at a 33% CAGR over the past five years, and 41% CAGR over ten years, that won’t cut it with Cathie Wood.

Third, it’s now become clear that FB is facing headwinds on monetizing user impressions that will result in a 8-10-point headwind to its flagship advertising business. That’s probably a combination of the iOS privacy change that kicked in last year plus rising competition from TikTok. On top of all of that, there is some noise that Meta may have to pull Facebook and Instagram from Europe (where it has 15% of its daily active users) if it is unable to keep transferring user data back to the U.S., all a part of an ongoing spat between US and European data privacy regulators.

After Q1’s earnings, growth investors have lost faith in FB’s growth prospects. And the timing couldn’t have been worse given that those investors were already feeling battered by the tech rout, so the selling was relentless.

Meta: The New Value Story

But here’s the positive news that should resonate with value-oriented investors: Meta is now trading at valuations that are lower than the bottom of the COVID crash.

Value investors look for a few things … cribbing from Benjamin Graham (the economist who wrote The Intelligent Investor and whose methodology inspired, among others, Warren Buffet):

- Cash flow from operations;

- Price / earnings ratios;

- A history of earnings growth / capital efficiency;

- Minimal debt;

- Buying when recent sell-off / macroeconomic creates opportunities; and

- Buying and holding for the long term.

Graham’s broad principles are still how most investors make investment decisions in America’s $20 trillion stock market.

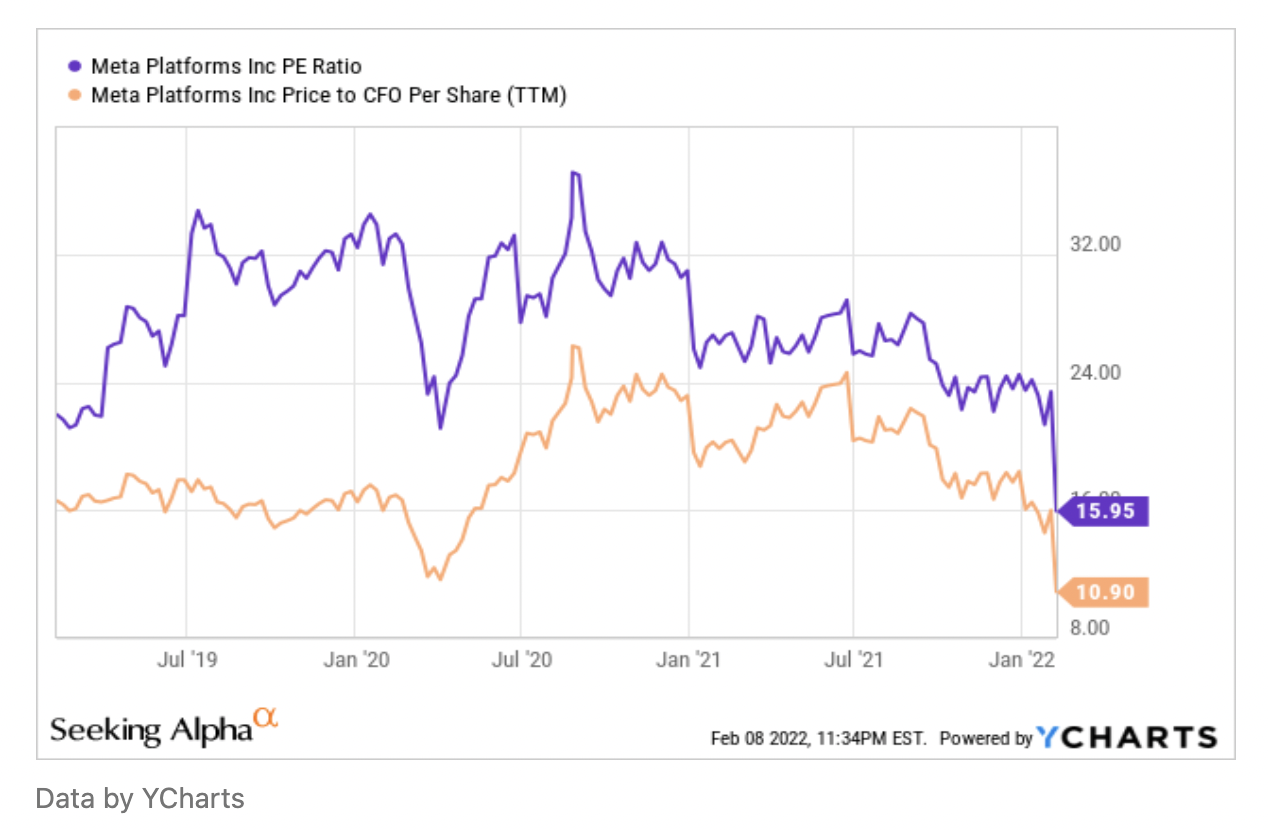

Meta is now trading at a price / earnings ratio of about 16. On a price / cash-flow-from-operations metric, it’s an astonishing 11. That’s lower than it was at the bottom of the COVID crash, which only makes sense to me if everyone’s New Year’s resolution was to give up social media.

Chart 2: Meta Price: CFO

A Look at the Q1 Numbers

Revenues rose 20% YoY to $33.7 billion, beating estimates by $230.6 million. Because of the lower guidance, forward PE is about 17 (or 20% lower than the S&P 500) and forward price / CFO is 11. Annual revenues are expected to rise 12.4% in 2022.

Income from operations were $12.6 billion, flat year-over-year, which won’t cut it with the Warren Buffett crowd. However, the operating loss from Meta’s Reality Labs was $3.3 billion – this is the company’s AR / VR division, which includes all of the hardware initiatives such as Oculus, plus some other moonshot stuff. It is the “metaverse” business unit of Meta Platforms, Inc.

As a “value investor,” you never like to lose money on new ventures, but this is an optional investment, and if it doesn’t work out, they’ll just kill it.

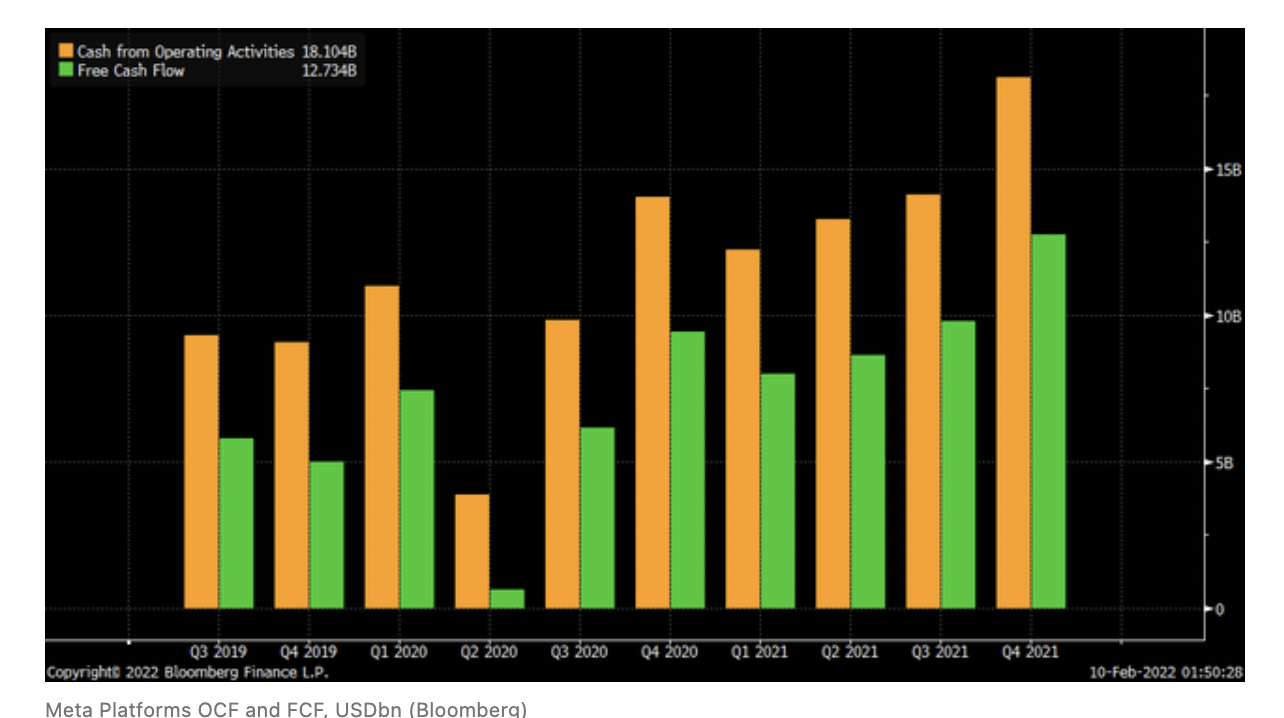

On the cash flow side, cash flows from operations were extremely strong. Operating cash flow rose to $18B, up 29% YoY. Furthermore, despite a surge in capital expenditures, free cash flow rose a whopping 35.1% y/y and 30.2% q/q to a record $12.7B.

FB is now trading with a 6.3% “free cash flow yield” (i.e., free cash flows from the business on a per share basis versus its market price per share. That’s four times Treasury yields and twice the rest of the NASDAQ 100.

Chart 3: Free Cash Flow Growth at Meta Platforms, Inc.

Conclusion

As Winston Churchill once said, never let a good crisis go to waste.

Buy Meta.