Introduction

A necessary, but awkward topic. It’s something that’s talked about in fragments for most and enviously for some. I’m talking about wealth, and today, in particular, a set of effective methods for building wealth observed across wealthy individuals in Silicon Valley.

Wealth is a means to fund a desirable quality of life for you and your family – a gateway to better education and healthcare, a tool to support the causes you care about, and ultimately, freedom. Unfortunately, it can also be a taboo subject between friends and family. Common knowledge is lacking and unbiased professional input is scarce. People can usually point to a few isolated cases of wealth creation (usually highly successful outlier cases), but connecting the dots of the process remains guesswork without a means to repeat successful actions.

I’m writing this guide as a general framework for readers, based on successful practices observed across high-net-worth clients I’ve had the privilege of serving over the years. It’s important to remember that everyone’s path to building wealth is unique and there is no “one size fits all” approach. Instead, my goal is to share some guiding principles that I’ve seen play out first-hand as a way to bring some clarity and insight to the broader population.

I’d like to break this guide into a few sections, with the expectation of going into greater detail at a later point in time:

- Equity & Risk

- Time Horizons

- Capital Allocation

- Tax Efficient Angel and Venture Capital Investing with ROTH IRAs

Overview

I’ve written this guide to be intentionally flexible, and in some cases, vague, so that it may be broadly applied. It is assumed at this point, that readers have a grasp of saving and budgeting. Prior to focusing on anything hereafter, it is important that you have:

- established yourself in a position where you can sustain a positive savings rate, and

- managed debt appropriately, including paying down all high-interest balances (i.e. student loans, credit cards, etc.). If that is not the case, I recommend installing Intuit’s Mint app (or any real-time budgeting assistant) and remaining focused on building a stable financial foundation.

Throughout this reading, keep in mind that there is no reliable get-rich-quick scheme. There is only a continuous series of tradeoffs and decisions, and the efficacy of your repeated decisions is what will determine your eventual outcome. We all know people who have gotten lucky, but luck is not a productive or repeatable goal. Lastly, no one starts from a perfectly even playing field — some people will need to work harder than others to achieve a similar outcome. Ignore distractions and remain hyperfocused on your own continuous improvement.

Equity & Risk

Equity and risk go hand-in-hand but are applied differently depending on the context for which they’re being used. Equity is a requirement for building wealth. Non-negotiable. There are two reasons for this:

- Firstly, there is an institutional imperative and corporate tailwind that seeks to maximize shareholder return (aka maximize wealth for owners of stocks), as opposed to maximizing the returns for other stakeholders (such as bondholders, cash compensation of employees, or taxes paid to state, local, and federal governments). Therefore, it’s rational to be aligned with this multi-trillion dollar tailwind and build equity.

- Secondly, capital grows faster than labor income. In the past 10 years, the inflation-adjusted median household income has only grown about 16%. On the other hand, the cumulative returns over the past 10 years for the Dow Jones, S&P 500, and NASDAQ have been+165%, +203%, and +478%, respectively.

Equity can be accrued in many forms, but is primarily acquired in three ways:

- Purchased equity through open or secondary markets (i.e. common stock via an exchange or interest in private companies through rounds of financing);

- Equity ownership by means of employment (i.e. Incentive Stock Options, Non-Qualified Stock Options, or Restricted Stock Units);

- Gifted/ Inherited Equity — we will not be focusing on this, as it is out of our control.

In Silicon Valley, there is an extreme emphasis on points #1 or #2 of the above, with additional support from the alternate. Typically, #2 precedes #1, so we’ll start there.

To double-click on point #2, those looking to compound assets at a high growth rate typically target the equity of early-stage companies — mostly private — with higher fundamental business risk. Attaching your labor and earnings to the equity of a mature company like Procter & Gamble or Walmart is not a bad thing, but the prospects of growth (and therefore your wealth) are lower since their days of initial growth, adoption, and risk are well behind us.

Conversely, early-stage companies can grow 10x, 100x, 1000x, or more, but the probability of a successful exit (acquisition or public market listing) is low. Generally, the younger the company is, the lower your chances are of capturing returns, but the payoff will be much greater if you do. It is important to internalize these risks and dissuade yourself from becoming overly-attached to an early-stage company just because you have joined or invested. As a reference point, professional early-stage investors allocate capital across dozens of companies or more, expecting that most will fail, but a small few will provide sizeable enough returns to offset losses and provide a meaningful gain. You should approach this type of employment with a similar mentality.

Asset growth through equity-based compensation falls into three categories. The suitability of each will need to be adjusted for your personal situation and tolerance for risk:

- Serial start-up employee or entrepreneur: very high risk and reward; no visible path to a liquidity event or possibly even material revenue traction; expect to join or start multiple companies before seeing sizeable equity payout (if ever); difficult to de-risk through analysis; significant personal time commitment and uncertainty. It is common for employees in this category to vest most of their equity (usually a 4-year timeline) and leave to join another startup unless the traction is promising. In this way, they are able to build their own portfolio of early-stage equity through employment.

- Mid- to Late-stage private company: mid to high risk and reward; some form of visible path to a liquidity event (though not at all guaranteed); easier to de-risk decision by joining a company with strong traction and notable backers (i.e. Sequoia, Founders Fund, Benchmark Capital, Accel, Greylock Partners, etc.). Backers of such companies can all be found here.

- Growth-oriented public company: lower risk and high variance in reward; immediate liquidity available as equity vests monthly or quarterly; publicly available financials and analysis available to gauge business risk; generally the least impacted by exogenous events; the most stable work-life balance of the three categories.

Most successful people will find one particular area that best speaks to their skill set, personality, and risk tolerance, and continuously seeks growth in expertise for that specific category. For example, a salesperson who is excellent at developing new, creative avenues to find customers might be best suited to category #1, whereas someone who thrives with stable processes, guidance, and support might be better suited to category #3.

On a closing note for this section, it is extremely important to focus on the potential of the company you are joining, and not your title. Giving yourself a “demotion” in exchange for equity in a successful early-stage company is better than being a Senior VP of a company that goes belly-up.

Time Horizons

The concept of time horizon is important in bridging the gap between both the preceding section of equity ownership and risk, and the subsequent section regarding capital allocation. Regardless of your own intention to accept more risk, if you misalign capital and time horizon, you are gambling. Understanding time horizons and capital requirements are essential, as adjustments over time reduce your margin of error, the range of potential outcomes, and a large degree of uncertainty.

To contextualize further: if you have a short time horizon for capital needs (e.g. less than 3 years) but allocate too much capital to risky assets, like technology stocks, volatility can lead to short-term loss of capital, leaving you underfunded. Comparatively, if you have a long time horizon, but allocate too much capital to low-risk assets, such as CDs and Treasuries, you forego a higher rate of compounding, also leaving yourself exposed to potential underfunding.

The way we think about time intervals can be segmented into five different categories, each with its own set of viable asset classes:

White text denotes asset classes that apply to accredited investors (or above) only. See SEC definitions for investor qualification definitions. The mentioned asset classes do not represent an exhaustive list and are merely a few examples that pertain to each category.

Again, this illustrates a general barometer for how capital might be allocated to satisfy different time horizons and liquidity needs. There are, of course, exceptions to each of the above categories and this should be adjusted to each individual’s personal situation. In the context of our discussion today, we are concerned about focusing entirely on the highlighted “Wealth Expansion” section above.

Across the clients who have successfully and continuously grown their wealth, the goal remains clear: maximize capital allocation to Growth and Aggressive Growth while maintaining a minimally viable amount to satisfy short-term obligations.

In the next section, we will explore two successful models that meet the above framework.

Capital Allocation

After capital for short-term obligations has been earmarked and separated from long-term capital, we can start to think about how to craft a portfolio to optimize growth. However, the details of capital allocation and portfolio modeling far exceed the capacity we have today, so I will try to dilute those learnings into two common templates. Both models assume, at this point, that you have some excess capital on your personal balance sheet — either through the accumulation of cash savings or through company equity. This includes savings both in and outside of employer-sponsored retirement plans. However, investment options through 401(k), 457, and 403(b) plans are typically more limited.

The first can be applied to non-accredited investors and the second to accredited investors.

An accredited investor is defined as persons who meet one of the following criteria:

- Single taxpayers with income in excess of $200,000 the past two years who expect such income to exceed this threshold in the current tax year;

- Married taxpayers filing jointly with income in excess of $300,000 the past two years who expect such income to exceed this threshold in the current tax year;

- Either single or married persons who have a net worth of $1 million or more, not including their primary residence.

The primary difference between the two is that accredited investors have a wider lens of available asset classes, which are generally more complex, riskier, and can be associated with longer time horizons. It should be the goal of the non-accredited investor to either raise income or grow assets to meet the accredited threshold as soon as possible.

In both models — I cannot stress this enough — do not try to time the market. This applies to both the purchase of securities and the tendency to sell during tumultuous markets. Identify high-quality, long-term positions and continue to add assets to them as regularly as possible. Those who successfully grow their wealth recognize that this is a marathon, not a sprint. The adage “time in the market is more important than timing the market” holds true.

Model 1 — Non-accredited Investor (public market focus)

In the first model, we focus entirely on public market equities as a means for growth, since the investor has not yet obtained accredited status.

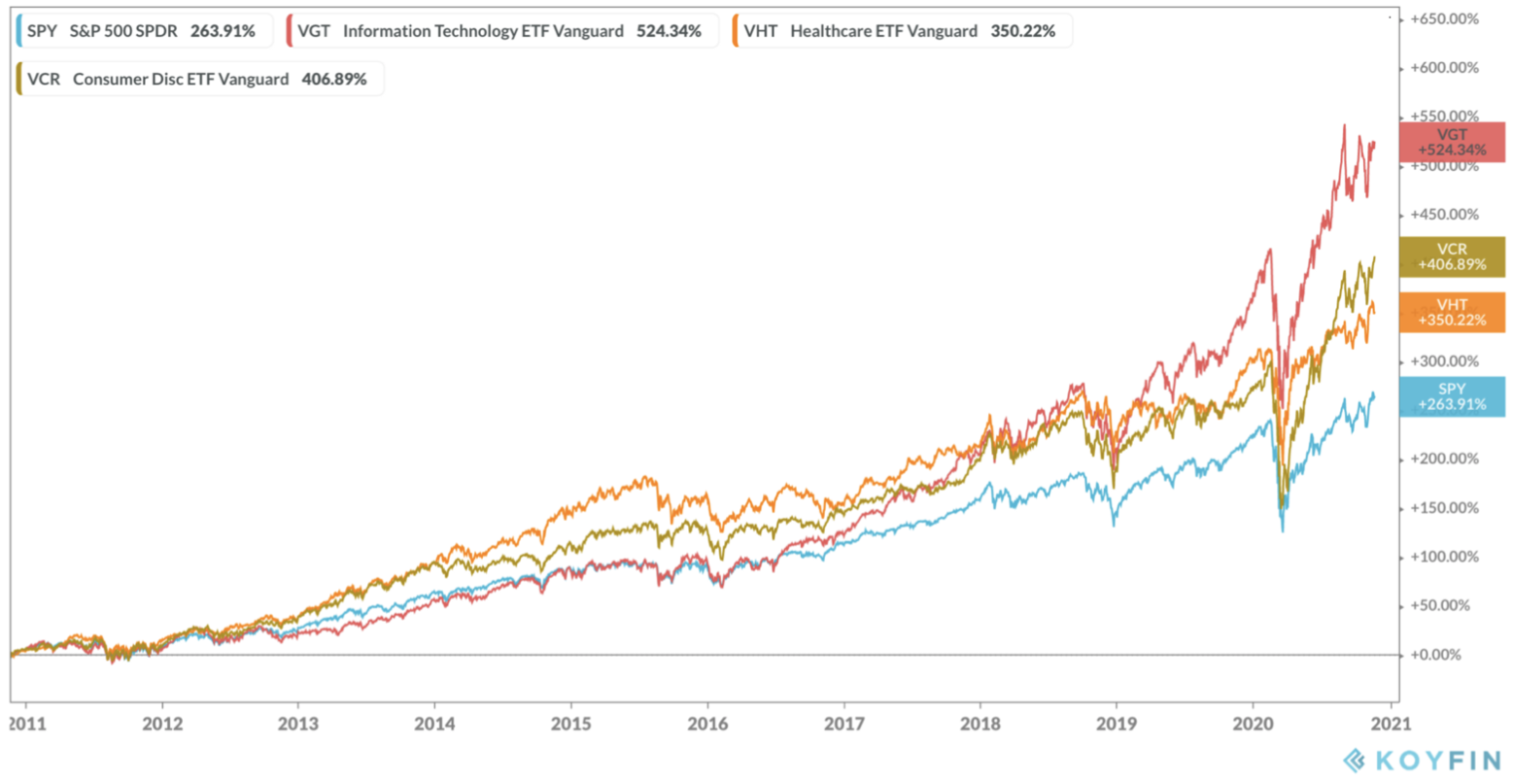

As shown below, more emphasis is placed on growth-oriented themes such as technology, healthcare, and consumer discretionary sectors. These three sectors, over time, have delivered more significant total returns than the other eight market sectors. As we look towards future growth and innovation, I believe this will hold true in the coming years as well. The primary objective for including these themes is to increase the total cumulative return irrespective of short-term volatility, ultimately leading to a higher average rate of compounding. We will explore the benefits of such themes further in just a moment.

Interpretation of chart: the sum of the two categories Growth Themes and Core Postion should equal 100% and is separate from cash and short-term assets balance.

When constructing your portfolio, it’s imperative that you’re honest with yourself about:

- Your own sophistication – how well you understand the characteristics of different asset classes, their relationship to a changing economic cycle, the mechanics of different investment vehicles, and the risks associated with each.

- Level of interest – Without a meaningful level of interest, investing will fall lower on your list of priorities and the portfolio’s returns can be impaired as a result.

- Available time to manage – some people have a high level of interest and sophistication, but if you have a very demanding schedule, without sufficient time to monitor your positions, investing using a more passive approach can make sense.

If you have doubts about any of the above, your best possible options are to either use diversified, passive funds (mutual funds or ETFs) that require very little maintenance, or hire a professional. If you feel compelled to take a hands-on approach to learning and the above criteria are not met, I recommend separating a “play account” with 5% of total assets to practice, test your hypotheses, and build confidence.

In most cases, successful clients have focused their time on professions and either delegate asset management or invest in positions that don’t need to be frequently monitored — predominantly ETFs with a small few, high-conviction stocks of companies personally known to them.

I’ve included the two charts below to specifically illustrate:

- Risk (volatility). In this particular case, the risk of allocating more capital towards sectors such as technology, healthcare, and consumer discretionary. Note the steep decline in value in early-2020 during the COVID breakout. During these times it is important to maintain a long-term focus and remember that volatility is a recurring feature of this type of strategy.

- The benefit of compounding. In the table below you’ll notice that the delta in Compound Annual Growth Rates (CAGR) ranges from 2.44% to 6.30%. However, over a 10-year period, that delta — if consistent — translates to a difference of 86% to 260% in total return. While differences may seem small on a year-to-year basis, those effects are magnified substantially over the years, if sustained. This is true of both positive and negative decisions.

In the second model, we will be building on model 1 with specific additions to asset classes in the private market space.

Model 2 — Accredited Investor (private market focus)

Compared to the former model, this section will be entirely devoted to capital allocation in private markets. Results can vary greatly in this space depending on access to certain managers and the fees that result from such access. The purpose of including asset classes found in private markets is to gain access to specialized or niche strategies with a competitive advantage over public market options. These asset classes should satisfy one of the following characteristics:

- Uncorrelated, positive returns (diverse sources of appreciation or income whose values move independently to public market assets)

- Correlated, excess returns (through the use of leverage, complex mechanics, or access to attractive, supply-constrained opportunities)

Interpretation of chart: the sum of the two 40-60% weighted categories should equal 100% and is separate from cash and short-term assets balance.

In particular, I’d like to highlight early-stage venture capital (angel, pre-seed, or seed investing), as this area has provided the greatest asymmetry and outsized returns that I have observed to-date.

Early-Stage Venture Capital — Angel and Seed Investing

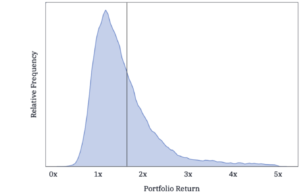

As mentioned previously in the “Equity & Risk” section, professional investors in the early-stage venture space fully anticipate that most companies in their portfolio will fail. A small handful will have a decent return, but not stellar, and one or two will be successful enough to offset any losses and still provide a compelling total return on invested capital. Famously, as the first investor in Facebook, Peter Thiel turned $500,000 into roughly $1.1 billion (a 2200x return).

In successful early-stage funds, there is a significant skew in returns towards one or a few companies, to which the majority of the fund’s gains can be attributed. Below is a hypothetical illustration from AngelList on what the distribution of those returns might look like. It’s also a very good depiction of how difficult it is to yield outsized returns, and the need to cast a wide net.

One of the most difficult elements — especially for those who are not connected in the technology community— is getting a consistent deal flow of high-quality startups. A commonly used tactic is to “spray and pray,” or invest smaller principal amounts in a larger number of companies (i.e. 100+), as opposed to being more concentrated (i.e. <50). Without a track record of investing in early-stage companies, and the ability to quantify the success of your judgment, this is the preferred technique.

In order to source deals, an effective way to participate is through a syndicate as a co-investor. A few popular syndicate programs are:

- Jason Calacanis’ The Syndicate

- AngelList Syndicates (better thought of as a marketplace for various angel investors)

- Tribe Capital’s Firstlook program

This is an incredible way to delegate deal-sourcing for those of us who have full-time jobs and a less impressive network of founders and talent. Many syndicates charge a 20% carry, but splitting the profits 80/20 is a very reasonable price to pay for regular deal-sourcing from a pool of great talent.

While others in Silicon Valley have a network of dozens (or more) of talented engineers, operators, and entrepreneurs, most people lack access to such resources and it makes sense to pay to play.

Tax Efficiency & Optimization

We always want to think about allocating capital through the lens of the question “what’s the net to me?” Especially in high-tax states like California, half of any potential gains can end up in the pockets of the IRS and the Franchise Tax Board. So, while your gross gains might look very impressive, only taking 50% home might dissuade you from making certain capital commitments in the first place. Today, there is one key concept I want to cover, that if utilized effectively over time, can make an unbelievable difference.

Asset Location — Roth Conversion & Utilization

Asset location is a less well-known concept than her close sister, asset allocation. While asset allocation deals with a mix of a portfolio’s asset classes (stocks, bonds, cash, etc.), asset location specifically focuses on the types of accounts in which those asset classes are placed. In a perfect world, we could allocate all of our high-growth assets to Roth accounts, where earnings grow tax-deferred and can be distributed tax-free as long as you’re 59 1/2+.

Accredited investors are unlikely to meet the Roth IRA contribution threshold since the income limits are <$206,000 for married filing jointly and <$139,000 for single tax filers in 2020. Even if you’re under the income cap, contributions are limited to $6,000 ($7,000 if you’re 50+). However, you are still able to do a Roth conversion from a Traditional IRA at any point in time — as much as you like, whenever you like. You pay income tax on the full amount that’s converted, but earnings can grow tax-free thereon out. The sooner this conversion happens, the more post-tax alpha can be realized.

Take our previous example of using The Syndicate for angel investing — you’re able to convert assets from a Traditional IRA (i.e. an old 401k that was rolled over) to your Roth, and then make a direct investment through a service like Alto IRA, Pensco, or Millennium Trust (an intermediary trust company needs to facilitate IRA investments into private vehicles). If you hit it out of the park with an investment of $25k that turns into $5 million, for example, all of those earnings could be realized and reinvested untaxed. Given that early-stage investing entails a small capital outlay upfront with the possibility of achieving outsized returns, it is the perfect candidate for a Roth IRA.

Keeping this concept in mind over years to come, especially in years when income is in lower tax brackets, will allow you to take advantage of more tax-efficient modeling. To illustrate, an investment of $50,000 into Apple 15 years ago would be worth roughly $3.5 million today.

If this investment was made in a regular brokerage account, tax liability would be up to 20% + state taxes. $1.15 million for a CA resident. Were the same investment made through a Roth IRA, you would have an additional $1.15 million to distribute to yourself tax-free and use as you please.

Closing Remarks

While I hope this has provided readers with a few tangible action items to improve their long-term financial outlook, it is neither an exhaustive nor a comprehensive list. If executed consistently, these few foundational building blocks can significantly improve a long-term outlook on wealth from where most people stand today. To reiterate very briefly:

- You must own equity to build wealth, and thoughtful placement and allocation of equity will lead to greater profitability of future outcomes.

- Do not gamble with short-term assets. Build a stable base and then expand outward to capture future opportunities. It is not worth disrupting the incredible benefit of compound interest.

- Allocation matters. Opportunities to broaden allocation options come under the accredited investor umbrella. Get accredited and continue to follow through on a plan with high-growth conviction.

- Put your eggs in the right baskets. You will thank yourself for paying taxes forward now so you don’t need to pay them on earnings later.

In the current environment of Robinhood traders and the proliferation of speculative options bets, it is important to remember that consistency, commitment, and repetition of proven successful tactics will likely have a far more meaningful impact on your ability to build and sustain wealth.

To provide a final few guiding principles from one of my favorite entrepreneurs and investors, Naval Ravikant:

- Ignore people playing status games. They gain status by attacking people playing wealth creation games.

- You are not going to get rich renting out your time. You must own equity — a piece of a business — to gain your financial freedom.

- Pick an industry where you can play long-term games with long-term people.

- The internet has massively broadened the possible space of careers. Most people have not figured this out yet.

- Play iterated games. All the returns in life, whether in wealth, relationships, or knowledge, come from compound interest.

- Do not partner with cynics and pessimists. Their beliefs are self-fulfilling.

Please share this with anyone who you think might be able to benefit from its contents, and let’s get everyone to a more financially secure world. This post originally appeared on Sean’s Medium blog.